Asian Dividend Gems: Tingyi Holding

Asian Dividend Gems: Tingyi Holding

Shares of Tingyi Holding are oversold. It has high dividend yield and attractive valuations. Its core instant noodles and beverage businesses are turning around this year.

Current dividend yield is 5.4%. Tingyi Holding's dividend yield averaged 5% annually from 2018 to 2022.

Tingyi's "Master Kong" instant noodle is one of the best known brands in China. The company is also one of the largest producers and distributors of beverages in China.

Conclusion First

Tingyi Holdings operates Master Kong instant noodle brand in China which is the number one in this category. Tingyi also operates one of the largest beverages businesses in China, capitalizing on its relationship with Pepsi. Tingyi's shares are down nearly 45% since the food scandal disaster in March 2022. It has continued to underperform Hang Seng index so far this year.

Nonetheless, Tingyi has millions of loyal customer base, attractive valuations, and high dividend yield and payout. In addition, after two consecutive years of declining net profit in 2021 and 2022, its net profit improved noticeably in 1H 2023. Important raw materials including palm oil and wheat (flour) prices which increased materially in 2021/early 2022 have been stabilizing/declining this year which should help the company's profit margins. Therefore, we have a positive view of Tingyi Holdings in the next 1-2 years.

Tingyi Holding DPS, Dividend Yield, & Dividend Payout

Tingyi Holding's dividend yield averaged 5% annually from 2018 to 2022. Its annual dividend payout averaged 99.5% in the same period. Although the company's dividend yield has been relatively high in the past five years, its DPS has been wide ranging from the low of HKD 0.50 in 2018 to HKD 0.86 in 2020. Current dividend yield is 5.4%.

Tingyi Holding Earnings & Dividends (Source: Smartkarma)

Tingyi Holding Company Background

Tingyi Holding (322 HK) specializes in the production and distribution of instant noodles and beverages in the PRC. Tingyi Holding currently has a market cap of 57.3 billion HKD (US$7.3 billion). The company was founded in 1992 and is headquartered in Shanghai, China. The company generates nearly 100% of its revenues in mainland China/HK. Tingyi has an exclusive relationship with PepsiCo to manufacture, bottle, package, distribute and sell PepsiCo soft drinks in the PRC.

It is estimated that Tingyi has about 46% market share in the instant noodles and 43% share in ready-to-drink (RTD) tea segments in China. Tingyi (through its relationship with Pepsi) also has about 32% market share in the carbonated soft drinks segment in China. The company's core products in the beverages segment include RTD (ready to drink) teas, carbonated drinks, juices, and coffee drinks/functional drinks/probiotics.

The company's instant noodles are mainly sold under the "Master Kong" brand which is one of the best known brands among consumers in the PRC. At the end of 2022, the company distributed its products throughout the PRC through its extensive sales network consisting of 337 sales offices and 322 warehouses serving 76,528 wholesalers and 254,975 direct retailers. Its extensive sales and distribution network is one of the reasons for the company's leading market position in China.

Strong customer loyalty - The company's products have strong brand loyalty among millions of people in China. According to the Kantar Brand Footprint Report in 2022, Master Kong had been ranked among the top three brands as first choice by Chinese consumers for ten consecutive years.

Tingyi Sales Office, Distribution Centers, Production Centres, and Employees (Source: Company data)

Chinese consumers more selective on purchasing higher priced food/beverage products - Post COVID-pandemic, millions of households in China are facing increasing pressure on their budgets. Although travel restrictions have been lifted in China, millions of customers are travelling less than prior to COVID. Due to cost of living pressures including higher interest rates (mortgage payments) and higher cost of food, fuel, clothing, and utilities, these millions of Chinese consumers have been more selective about the types of food they buy.

In this respect, instant noodles have been beneficiaries since they tend to be lower priced than some of the other food items such as dairy, meat, fruits, and vegetables. On the other hand, beverages have been negatively impacted as more Chinese consumers reduce spending on higher priced beverages.

Food delivery apps reducing demand for instant noodles? Ordering food in China has become very convenient in China with the tremendous surge in use of food delivery apps. This has been cited as one of the reasons why the Chinese consumers would not want to stock up on their instant noodles. We think that this is partly true. On the other hand, the instant noodles tend to be much cheaper than ordering food through apps. In addition, making instant noodles at home typically takes less than five minutes whereas you typically have to wait for 30 minutes or more to get your food delivered.

Stabilizing palm oil prices - After surging palm oil prices in 2021 and early parts of 2022, they have been stabilizing this year. Palm oil is used to cook instant noodles. Indonesia and Malaysia constitute 85% of the world's palm oil supply followed by Nigeria, Thailand and Colombia. Stabilizing palm prices should have a positive impact on Tingyi's instant noodle business. However, a key outlier is what would happen in the ongoing war in Israel. A prolonged war involving numerous nations and significantly important regions/countries in the Middle East could have a major impact on crude oil prices as well as crude palm oil prices.

Declining wheat prices - After all time highs in wheat prices in May 2022, wheat prices have fallen by nearly half. Wheat is used to make flour which then is processed to make instant noodles. Lower wheat and flour prices should have beneficial impact on the profitability of the company's instant noodle business.

Wheat prices trend (Source: https://tradingeconomics.com/commodity/wheat)

Sugar prices continuing to rise - Sugar is an important raw material for its beverages as well as instant noodles. Unlike wheat and crude palm oil, sugar prices have continued to increase in the past two years. Higher sugar prices have resulted in higher raw material costs especially for the company's beverage products.

India, the world's largest sugar producer and second largest exporter, has continued to restrict exports since last year. In addition, the sugar production in Europe declined on lower beet crops derived from reduced acreage and severe summer drought in 2022. The output is set to rise in Brazil, but the higher sugar cane supply is likely be allocated to ethanol. Furthermore, the fluctuating oil prices impact the changes in sugar prices as well.

Sugar price trend (Source: https://tradingeconomics.com/commodity/sugar)

Revenue Breakdown (By Business Segment) - The company's business is broken down mainly into three segments including beverages, instant noodles, and instant food/others. In 2022, beverages accounted for 61.4% of total sales, followed by instant noodles (37.6%), and instant food/others (1%).

Source: Smartkarma

Master Kong instant noodles (Source: Company data)

Beverages sold by Tingyi in China (Source: Company data)

Tingyi Holding Major Shareholders

Wei family and Sanyo Foods are the largest shareholders as each owns 33.42% stake in the Tingyi Holding. Other major shareholders include Genesis Investment Mgmt (1.73%), Vanguard (1.66%), Blackrock Fund Advisors (1.16%), and Capital Research & Mgmt (1.1%).

Food Scandal Disaster in 2022

Tingyi faced a major food scandal disaster in 2022. China Central Television exposed food safety problems at one of Master Kong's suppliers of suan cai, or Chinese sauerkraut, in March 2022. Afterwards, Tingyi's share price plunged. Tingyi's share price reached its highs in the past five years on 18 February 2022 when it reached HKD18.04 per share. Since then, Tingyi's share price has fallen 44%.

After this incident, Tingyi promptly suspended its relationship with this problematic supplier. However, the damage was already done and it has soured its brand image among millions of customers in China. More than a year and half have gone by since this food scandal erupted. Although the company lost many customers after this food scandal disaster, it has recovered some of the lost market share with superior products and emphasis on food quality.

Key Financials

Despite solid high single digit sales growth from 2020 to 2022, the company's profit margin declined in this period. EBIT margin declined from 9.9% in 2020 to 5.8% in 2021 and 4.7% in 2022. The major reasons for worsening profit margins were due to higher raw material costs and other costs including logistics and labor. The company raised product prices on many of its instant noodles and beverages in 2021/2022. However, the overall higher costs (including raw materials, logistics, and labor) increased at faster pace then the product price hikes in this period.

Nonetheless, the company's profit margins have been improving this year. The consensus estimates the company's EBIT margin to improve from 4.7% in 2022 to 6.5% in 2023 and 7.4% in 2024. The company's ROE averaged 18.5% from 2020 to 2022. The consensus estimates its ROE to improve to 26.2% in 2023 and 32.4% in 2024.

In 2022, the company's revenue increased by 6.3% YoY to reach 78.7 billion RMB. The revenue from instant noodles grew by 4.2% YoY and revenue from beverages increased by 7.9% YoY. Gross margin declined by 1.3 percentage points YoY in 2022. The company also had higher distribution costs to revenue which rose by 0.15 percentage points in 2022. In 2021 and 2022, the rising prices of bulk raw materials negatively impacted the profitability of the company. The COVID pandemic also restricted the mobility of the people in China and reduced demand for some of the company's food products including beverages.

In 2022, the company's instant noodle business generated revenue of 29.6 billion RMB, accounting for 37.7% of its total revenue. Gross margin of the instant noodles decreased by 0.41 percentage points YoY to 23.95%, due to higher raw materials prices and shift in product mix.

Tingyi Holding Revenue, Net Income, & Net Margin (Source: Smartkarma)

Tingyi Holding Gross Profit & EBITDA (Source: Smartkarma)

1H 2023 Results Comparison - Tingyi Holding had revenue of 40.9 billion RMB (up 7.1% YoY) and net profit of 28.9 billion RMB (up 28.9% YoY) in 1H 2023. Revenue from instant noodles increased by 3.0% YoY and revenue from beverages increased by 9.5% YoY in 1H 2023.

After decline in net profit of the company for two consecutive years in 2021 and 2022, the company's profits have started to turn around in 1H 2023. During 1H 2023, the gross profit margin of instant noodles increased by 5.20 percentage points year-on-year to 25.8%, due to favorable selling prices and raw material prices. In 1H 2023, the gross profit margin of beverage unit increased by 0.52 percentage point YoY to 32.7% due to favorable raw material prices and product-mix.

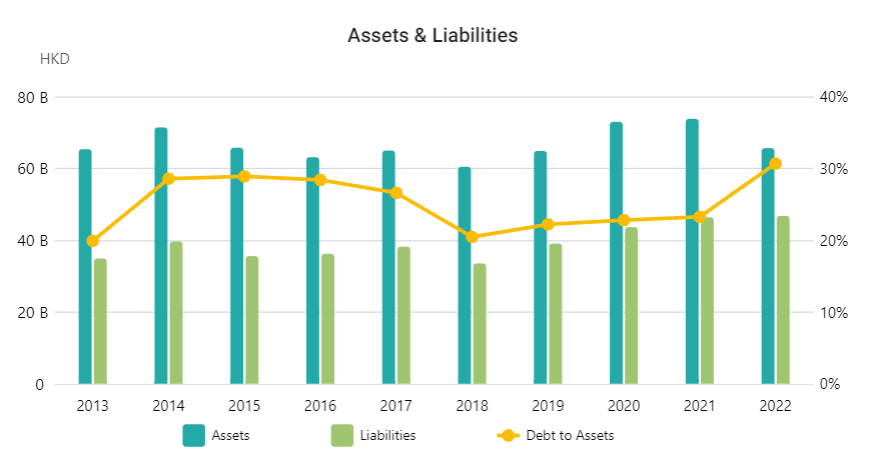

Balance Sheet Analysis -Tingyi Holding has a moderately leveraged balance sheet. It was in a net cash position at the end of 1H 2023. However, debt ratio was 279% at the end of 1H 2023, which is relatively high. The company's debt ratio increased from 169% at the end of 2021 to 248% at end or 2022 and 279% at end of 1H 2023.

The increasing debt ratio was caused by a combination of higher total liabilities and declining equity. Total liabilities rose from 37.9 billion RMB at end of 2021 to 43.7 billion RMB at end of 1H 2023. On the other hand, equity declined from 22.4 billion RMB at end of 2021 to 15.7 billion RMB at end of 1H 2023.

Tingyi Holding Assets, Liabilities, and Debt to Assets Ratio (Source: Smartkarma)

Cash Flow Statement Analysis - The company has a consistent record of generating positive cash flow from operations. Its free cash flow has been more sporadic. In the past decade, the company had positive free cash flow from 2016 to 2020. However, its free cash flow turned negative in 2021 and 2022.

Tingyi Holding Key Cash Flow Statement Items (Source: Smartkarma)

Tingyi Holding ROA, ROC, and ROCE (Source: Smartkarma)

Tingyi Holding Valuations

Tingyi Holding has attractive valuations. It is trading at EV/EBITDA of 6.8x and P/E of 15.5x. Its EV/EBITDA valuations have ranged from 6.4x to 17.2x in the past ten years. Its P/E valuations have ranged from 16.3x to 40.6x in the past ten years. On both EV/EBITDA and P/E valuations, Tingyi's shares are trading close to its 10 year lows.

Tingyi Holding EV/EBITDA Valuation Multiples (Source: Smartkarma)

Tingyi Holding P/E Valuation Multiples (Source: Smartkarma)

Disclaimer

The information contained on this website is not and should not be construed as investment advice. This insight is for informational purposes only and is not intended to provide financial, investment or other professional advice. It should not be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any security. Investors should make their own decisions regarding the prospects of any company discussed herein based on their own review of publicly available information.

The information contained on this website/newsletter has been prepared based on publicly available information and proprietary research. This insight does not contain and is not based on any non-public, material information. This publication makes no security recommendations whatsoever and is for educational purposes only. The opinions expressed in the publication are those of the publisher and are subject to change without notice. The information in the publication may become outdated and there is no obligation to update any such information.

The author does not guarantee the accuracy or completeness of the information provided in this insight. All statements and expressions herein are the sole opinion of the author and are subject to change without notice. It is highly advisable for you to do your own due diligence and invest at your own risk, independently of anything you may come across on this insight.

Any projections, market outlooks or estimates herein are forward-looking statements and are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Except where otherwise indicated, the information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and the author undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional materials.

This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Readers and recipients are requested to consult with professional legal, tax, accounting, investment advisors before making any investment decisions. No part of this publication may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed without the prior written consent of Douglas Research Advisory.

The author and the author’s affiliates may currently have long or short positions in the securities of certain of the companies mentioned herein or may have such a position in the future. The author does NOT accept any liability whatsoever for any direct or consequential loss arising, directly or indirectly, from any use of the information contained on this website/newsletter.